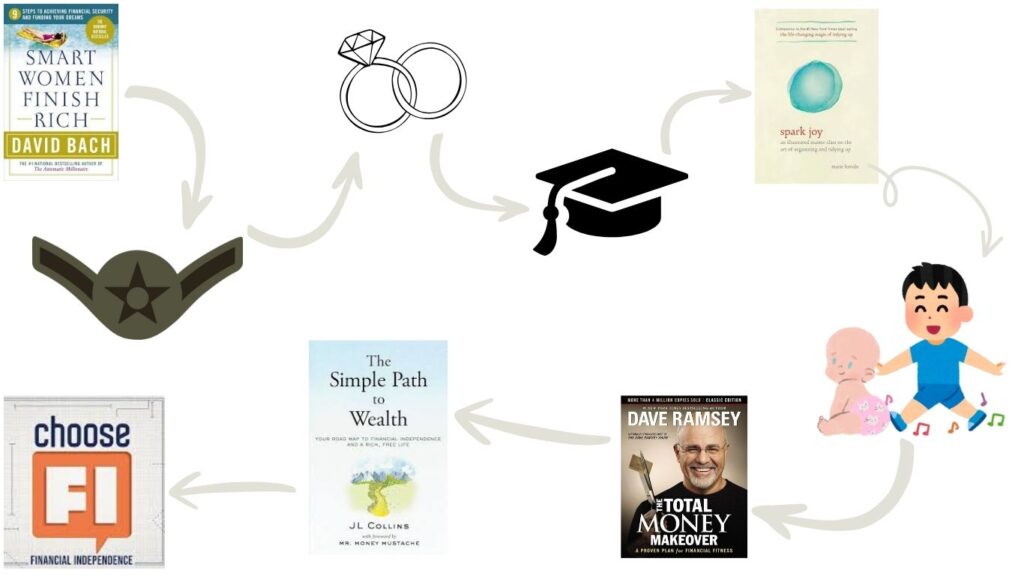

If you’ve read our “About” section, then you know that 1) Mr. Chill is the Servicemember and I am a civilian, and 2) we are just a few years away from retirement eligibility. I have had waxing and waning interest in personal finance over the years but was lucky to grow up with fiscally responsible parents – my Mom gifted me with “Smart Women Finish Rich” by David Bach in my early college years. Mr. Chill had what could be called – less of a good example? Not a good example? A bad example, okay.

While I generally recommend that you not get married young (although it has worked out great for us), there is a benefit in that you really are growing together – it’s the growing in the same direction or not that usually goes awry. And thankfully, we have grown together – building the life we want, which does have to include money.

So back to waxing and waning interest – my parents set the example young with allowance and expectations to save/spend/give. They paid for my first year of college (thanks Mom and Dad), but then I was married and we were on our own. Because I was pursuing professional school, Mr. Chill & I actually lived in 2 different states – which meant 2 different apartments, 2 different electric bills, 2 different water bills, yada yada yada and travel expenses to boot. Living on a lower enlisted salary and my very part-time job was not ideal, but was doable. We lived like college students, and it was fine.

When I graduated, we tackled my (>$100k) student loans with ferocity – as Dave Ramsey would say – using Dave Ramsey’s snowball method. I can’t stress this enough – if you have any amount of debt outside of a mortgage (or reasonable car loan), you should read and follow Dave Ramsey’s “Total Money Makeover.”

Unfortunately for us, once I was graduated and making real $, we fell victim to whole life insurance (which is semi-shocking considering Dave Ramsey’s stance on whole life). We were forking over $2-3k/month to fund our future retirement – that coupled with the aggressive student loan repayment, we barely had much leftover to even think about lifestyle creep.

Years later, when I was pregnant, Marie Kondo’s books went mainstream, or at least entered my world. I was holding every discount kitchen gadget and evaluating every piece of Ikea furniture I had acquired to determine what sparked joy. I ditched the food processor, random décor, along with probably 10 boxes worth of stuff in our tiny 3-bedroom base house. Minimalism, for me, is about having peace in my house and ability to focus my attention on what matters to me rather than cleaning and organizing all the time.

We did eventually go back to Dave Ramsey’s Total Money Makeover and got out of the prior whole life situation. At this point, we were 2 kids in, and had much less wiggle room (thanks to killer childcare costs). We cashed out (somehow) and had probably $150k to spare – we bought a car and started a brokerage account. Then covid hit. And we watched our account dwindle (thankfully it did recover).

This whole time, I was loosely budgeting – meaning I at least tracked our fixed expenses and tried with the flexible expenses, but certainly wasn’t tracking everything to the dollar. More recently, our kids got to a point where travel wasn’t awful – we were taking regular once or twice-yearly vacations when I recognized this as our single largest “want” expense. In comes travel hacking – this may be the most cliché financial independence journey ever. Now I was ready for the next step & we were now at a point where Mr. Chill’s retirement wasn’t some distant goal in the future that we would figure out someday – that someday is just around the corner. You know how they say, once you have kids, it all goes so fast – well it’s true. Anyway, so I’m starting to get anxious about hitting 20 years, and what will be our plan after. For his entire military career, when people would make mention of “Oh wow, he can retire in his early 40s,” I would reply with, “Yeah, but his retirement won’t be enough to live on.” And for a multitude of reasons, this could be very right or woefully wrong.

When I was early in my career, my older brother was feeling very jaded and looking for any way out of his engineering gig. I could not even fathom this – I went to school for all of these years and I loved it. My career has changed over the last decade plus, but really what has changed is my outlook on life. What I am seeing now is that I have two kids in elementary school, and I only have so much time left to spend quality time with them. It pains me to miss weekends, holidays, and school stuff. What weighs on me more heavily is just how stressful a (high stakes) full-time career is added on to all the normal duties of motherhood, and what I am so painfully aware of is that I am not the best me / mom / human I can be because of this stress. I want to give them my best. I have done enough therapy in an attempt to just make me a cool mom, but I guess it isn’t in the cards for me. So I’m pivoting my goals to retire when Mr. Chill does – in our early 40s. And now, we can circle back to our most recent dive into pursuing financial independence. This cliché journey continues where they all do – with J.L. Collins’ “A Simple Path to Wealth.”

We did not have any specific goals for our brokerage account, and mainly just watched it grow without intentionally adding to it. J.L. Collins’ easy, no-nonsense “VTSAX and Chill” approach and advice to invest in low-cost index funds struck a cord. We transitioned from investing with an advisor to simplifying our portfolio and managing it ourselves. His advice to prioritize freedom, not “stuff” truly aligned with our goals.

Wrapping up the cliché journey with our most recent fixation is the ChooseFI podcast. It finally felt like the pieces of my life were coming together to live with intention and focus on our priorities – choosing minimalism, living below our means, and chasing the freedom of FI. What I crave for life can be summed up in one word – simplicity.

A Timeline You Didn't Ask For