– header pin")

Is the juice worth the squeeze?

By now, I’m sure you’ve heard of FI – financial independence, and FIRE – financial independence retire early. Being around the military community for 17 years, I have seen many many many servicemembers come and go, and yet attended only a handful of retirement ceremonies. Which checks with the data – only about 10% of enlisted and 30% of officers make it to retirement. While I understand all too well the many drawbacks of military life, I just want to scream “don’t you understand how valuable a pension and health insurance forever is????” Alas, I do not yell. But, seriously, I want you to be able to truly weigh the benefits of Military Retirement if you are pursuing (or thinking about pursuing) FI.

I don’t know that I can actually order these without over-thinking it, so consider this to be – sort of – in no particular order. These will honestly need a deep dive post for each, so I’ll just sum it up here.

1. The Pension (& early $$)

Consider this to be the golden egg. There are 2 main reasons why the military pension is crazy beneficial for FIers. First, your FI number is calculated based on your annual expenses. Using the 4% rule, aka the rule of 25, if you have guaranteed income (ahem, the pension), you subtract that amount from your monthly expenses for your FI number. So:

Sorry Sap without a Pension with $100,000 annual expenses:

FI number = $100,000 x 25 = $2,500,000

Super Smart Servicemember who made it 20 years with a $60,000 pension and $100,000 annual expenses:

FI Number = $100,000 – $60,000 = $40,000 x 25 = $1,000,000

Your defined benefit pension (DBP) is worth millions. Literal millions. In this case, assuming a retirement age of 40 with a pension of $60,000 and a life expectancy of 78 years (average male life expectancy), it is worth $2.2 million ($60k x 38 years). So if you are currently 9 years in and deciding to get out at 10 years because you *know* you can make more money in the private sector, please see (future post).

Anyway, I said there were 2 main reasons the military pension is a golden egg. Here’s the other: your pension starts as soon as you retire. You don’t have to worry about bridging the gap from your desired retirement age (40-45) until age 59.5, when you can withdraw from traditional retirement accounts (401k, Roth IRA, Traditional IRAs) without a 10% early withdrawal penalty. Outside of pensions, the only other retirement account accessible at early retirement without penalty is a 457b (usually only available to teachers, firefighters, other government sectors).

2. Tricare

I can’t overstate how valuable access to Tricare is. The largest expense in retirement (outside of a mortgage) is usually health insurance. Medicare kicks in at 65 (but isn’t free), so most have to shell out-of-pocket from the desired retirement age (40-45) until 65. That’s a long time. Average cost of health insurance in the U.S. is $18,000 for family coverage and $13,000 for a couple. For a non-military FIer, assuming retirement at age 40 requiring 15 years of family coverage and 10 years of coverage for 2, total cost is upwards of $400,000 in the long run. Now compare that to our Super Smart Servicemember who made it 20 years and is retiring at age 40 – again assuming 25 years of coverage until Medicare – Tricare for retired military families is $744 per year x 25 years = $18,600 total.

Not to mention this also reduces your annual expenses for calculating your FI number. To afford an equivalent lifestyle, our Sorry Sap above has that $100,000 annual expenses + $18,000 annual health insurance cost = $118,000 for a more realistic FI number of $2,950,000 ($118,000 x 25).

3. VA DISABILITY

While not a guarantee, any VA disability you are awarded is non-taxable. Range is ~$7200/year (30% rating) up to $52,000ish (100% rating). VA disability is an earned benefit. We’ll talk more about it in a future post.

4. NON-TAXABLE INCOME (WHILE ACTIVE DUTY)

Non-taxable income includes (among others):

- Basic Allowance for Housing (BAH)

- Basic Allowance for Subsistence

- Cost of Living Assistance (COLA)

- Combat pay

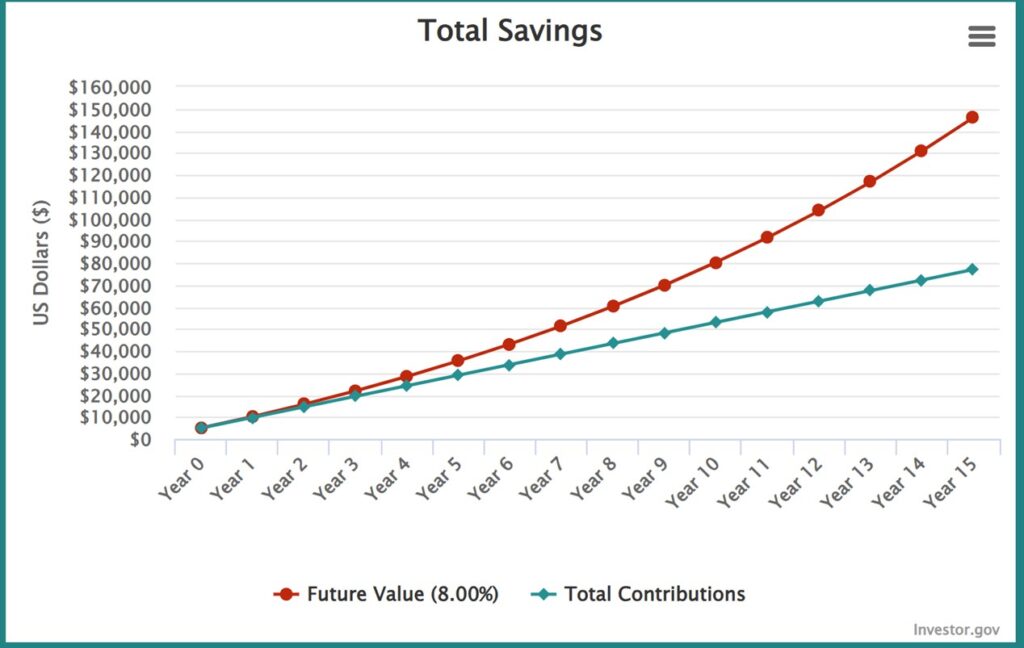

Using 1 example with BAH – an E-6 with dependents in Little Rock, AR gets $1833 per month in BAH. A civilian across the street paying the same mortgage has to earn that $1833 after tax. Your annual $22,000 BAH benefit would cost you almost $27,000 if it weren’t for the non-taxable advantage (assuming 22% tax bracket). Put that extra $5,000 savings in a brokerage account investing in the stock market and at 8% return, you have an extra $150,000 in your pocket after 15 years.

5. VA loan eligibilty (& house hacking)

The 0% down VA Loan can uniquely position servicemembers for a strong real estate portfolio. Even outside of house hacking, the VA Loan has other unique advantages.

other benefits to consider

These don’t make my top 5, but should also be considered. They just aren’t worth millions in comparison to traditional civilian benefits. Do not discount their power, though.

- GI Bill

- The Thrift Savings Plan (TSP)

“Your blog is titled TSP & Chill, and yet the TSP doesn’t even make your top 5 list for why military retirement positions you for FIRE?” Well, no, and here’s why – the TSP is essentially the 401k for federal employees, thus can be withdrawn like a traditional retirement account at age 59.5 (without an early withdrawal penalty). DOD will match contributions up to 5% under the Blended Retirement System (and you should absolutely always contribute at least up to the match). The catch is, they don’t start matching until 2 years in (essentially the vesting period).

The TSP does have low expense ratios (0.036-0.079%), but Vanguard Total Stock Index (VTI) has a comparable expense ratio of 0.03%. So, while the TSP is a useful tool, it is largely similar to retirement benefits in the traditional workforce, and not what I would consider to be uniquely positioning you for FI. We’ll dig deeper in a later blog post.

- Tuition Assistance (TA)

- Servicemembers’ Group Life Insurance (SGLI)

- Servicemembers Civil Relief Act (SCRA) and credit card benefits

- Cheaper tickets to Disney *funny face*

And now, you can compare and contrast these benefits with any actual or perceived downsides to active duty military service – years away from family, frequent moves, some utterly terrible assignments, lifelong anxiety, an emotional roller coaster of everyday life, general lack of autonomy and freedom, and the occasional existential dread.

It’s all about balance.

As for me and Mr. Chill, I guess we decided it would have to be worth it. Because we said so.

– footer pin")